6.1 모형 진단과 수정#

회귀분석 결과의 진단(diagnosis)이란 회귀분석에 사용된 데이터가 회귀분석에 사용된 모형 가정을 제대로 만족하고 있는지를 확인하는 과정이다.

잔차 정규성#

데이터가 모형 가정을 만족하면 분석결과로 나온 잔차는 정규분포를 따라야 한다. 예를 들어 다음과 같이 2차 비선형 관계를 가지는 데이터를 선형 모형으로 회귀 분석한 경우를 살펴보자.

def make_regression2(n_sample=100, bias=0, noise=0.3, random_state=0):

np.random.seed(random_state)

x = np.random.rand(n_sample) * 4

epsilon = noise * np.random.randn(n_sample)

y = x ** 2 + bias + epsilon

return x, y

x2, y2 = make_regression2()

plt.scatter(x2, y2)

plt.show()

dfX20 = pd.DataFrame(x2, columns=["X1"])

dfX2 = sm.add_constant(dfX20)

dfy2 = pd.DataFrame(y2, columns=["y"])

model2 = sm.OLS(dfy2, dfX2)

result2 = model2.fit()

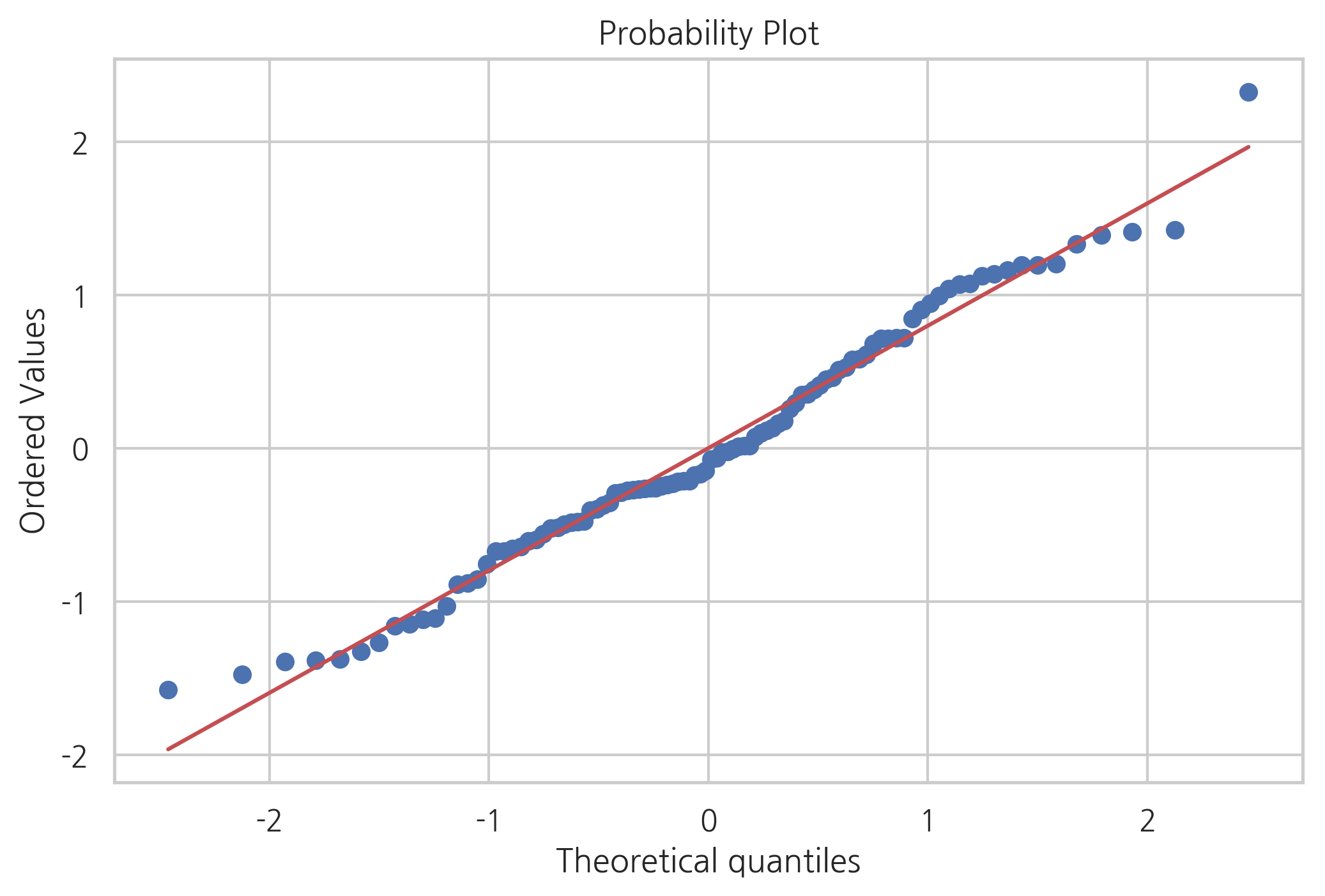

QQ플롯과 정규성 검정에서 보듯이 잔차는 정규 분포를 따르지 않는다.

sp.stats.probplot(result2.resid, plot=plt)

plt.show()

test = sm.stats.omni_normtest(result2.resid)

for xi in zip(['Chi^2', 'P-value'], test):

print("%-12s: %6.3f" % xi)

Chi^2 : 9.520

P-value : 0.009

잔차와 독립 변수의 관계#

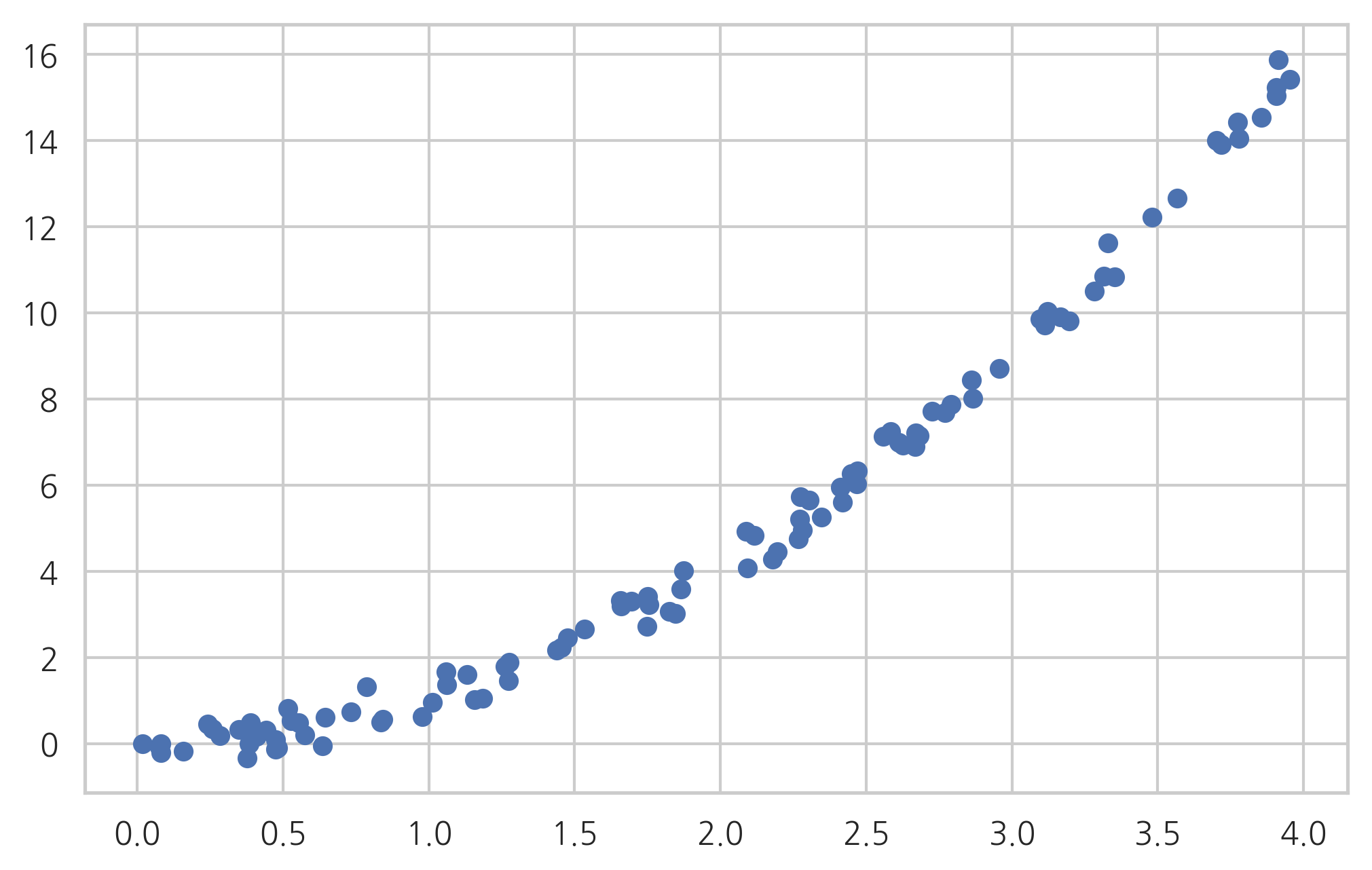

이번에는 또다른 데이터를 살펴보자. 이 데이터도 2차 함수 관계를 따르고 있으므로 선형 모형을 따르지 않는다.

def make_regression3(n_sample=100, bias=0, noise=0.5, random_state=0):

np.random.seed(random_state)

x = np.random.rand(n_sample) * 3 - 1

epsilon = noise * np.random.randn(n_sample)

y = x ** 2 + bias + epsilon

return x, y

x3, y3 = make_regression3()

plt.scatter(x3, y3)

plt.show()

dfX30 = pd.DataFrame(x3, columns=["X1"])

dfX3 = sm.add_constant(dfX30)

dfy3 = pd.DataFrame(y3, columns=["y"])

model3 = sm.OLS(dfy3, dfX3)

result3 = model3.fit()

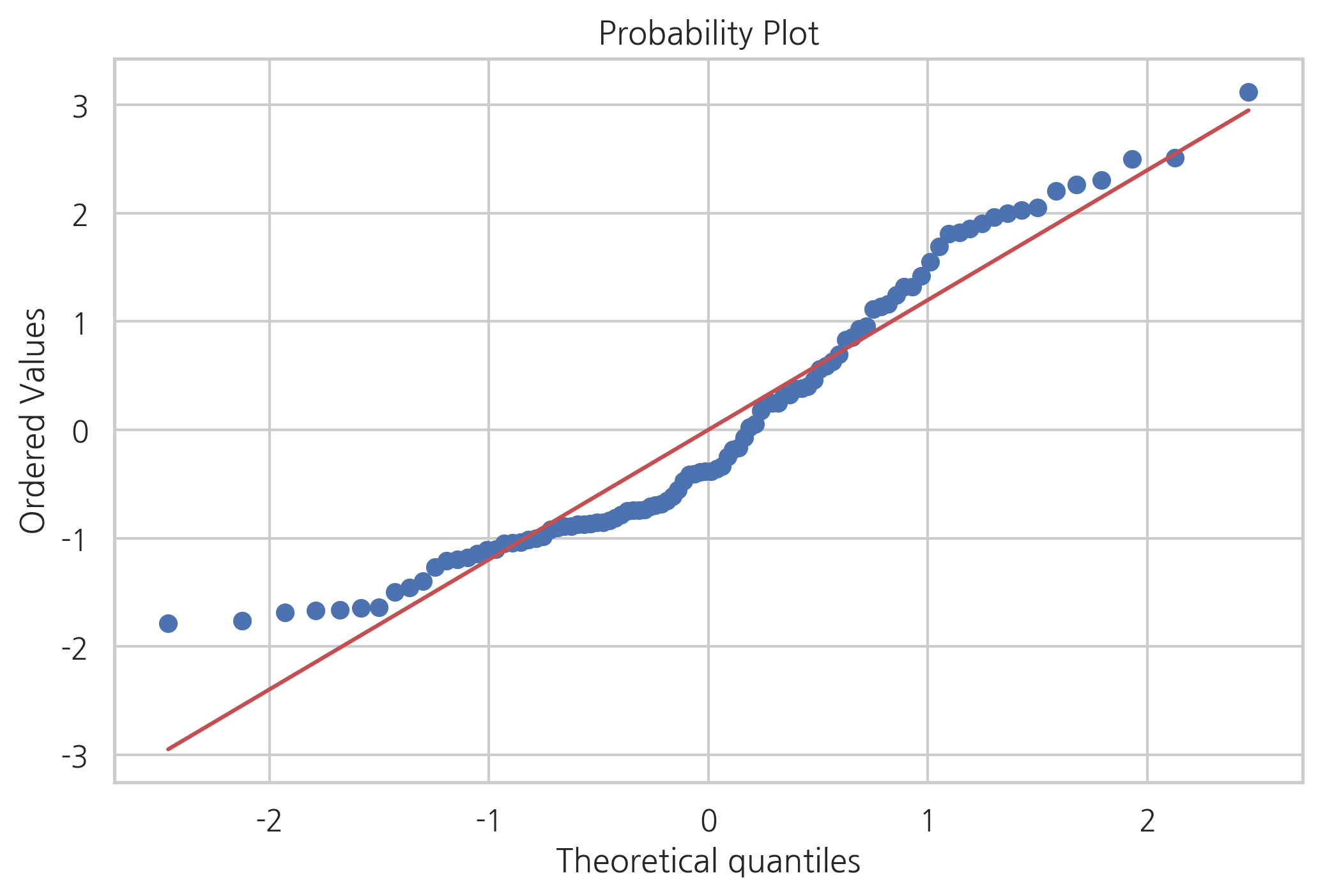

sp.stats.probplot(result3.resid, plot=plt)

plt.show()

test = sm.stats.omni_normtest(result3.resid)

for xi in zip(['Chi^2', 'P-value'], test):

print("%-12s: %6.3f" % xi)

Chi^2 : 1.202

P-value : 0.548

데이터가 모형 가정을 따르지 않지만 잔차는 정규 분포를 따르는 것을 알 수 있다.

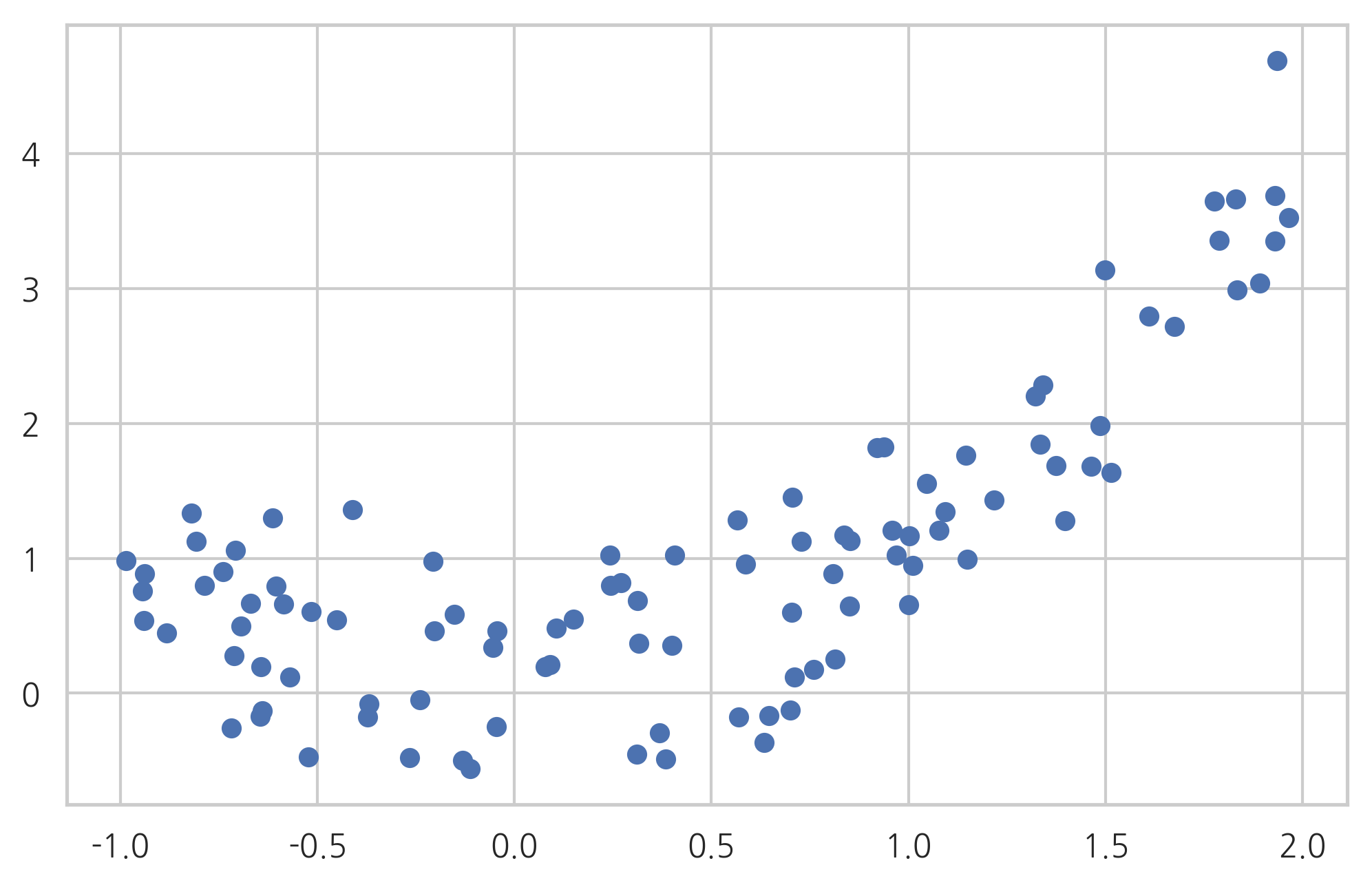

이러한 경우에는 잔차와 독립 변수간의 관계를 살펴보는 것이 도움이 될 수 있다. 데이터가 올바른 모형으로 분석되었다면 잔차는 더이상 독립 변수와 상관관계를 가지지 않아야 한다. 만약 잔차와 독립 변수간에 어떤 비선형 상관관계를 찾을 수 있다면 올바른 모형이 아니다.

다만 잔차와 특정 독립 변수간의 관계를 전체 모형이 올바른 모형이 아니라는 것을 알려줄 뿐이지 어떤 모형이 올바른 모형인지에 대한 정보는 주지 않는다.

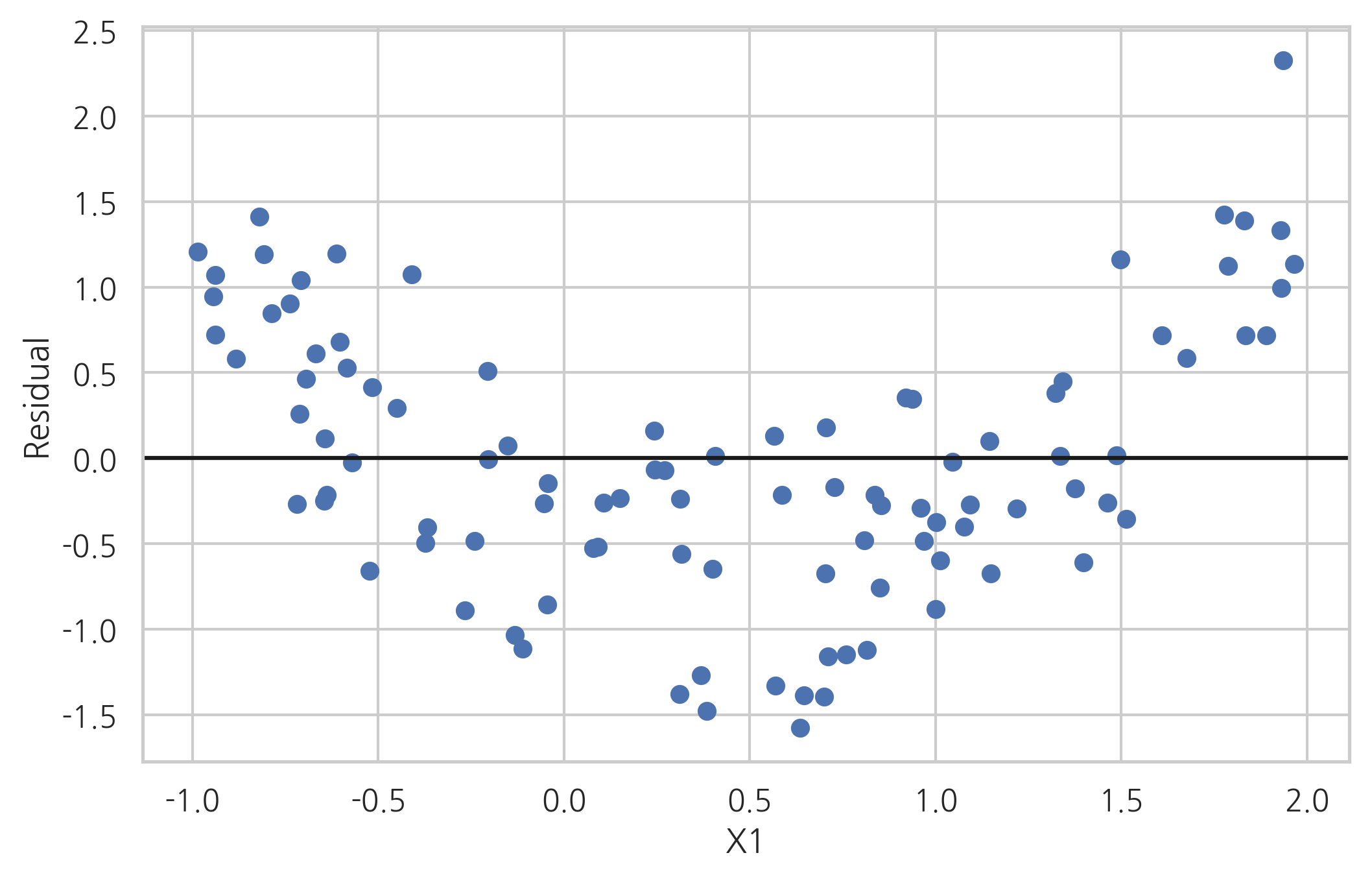

plt.plot(x3, result3.resid, 'o')

plt.axhline(y=0, c='k')

plt.xlabel("X1")

plt.ylabel("Residual")

plt.show()

이분산성#

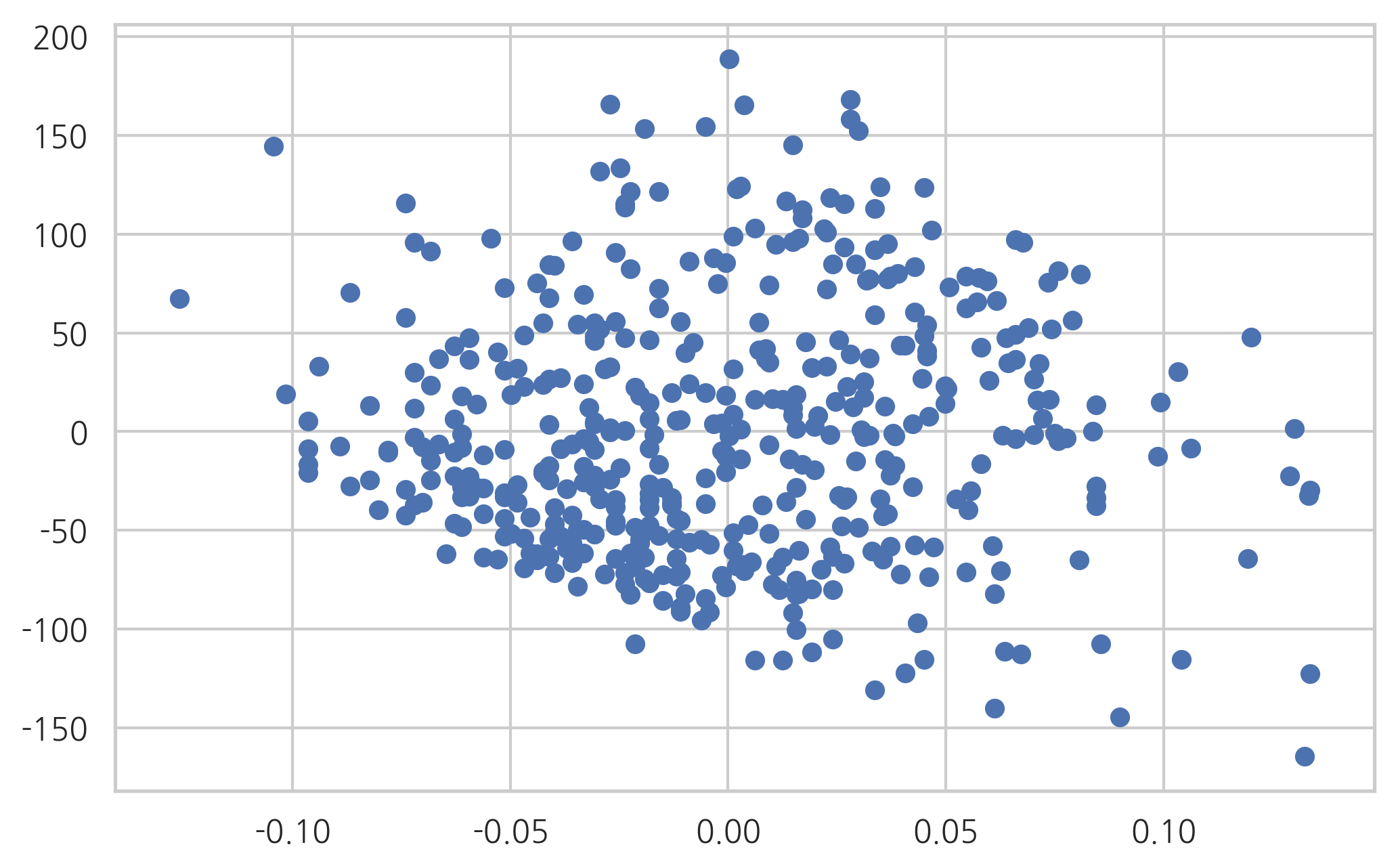

선형 회귀 모형에서는 종속 변수 값의 분산이 독립 변수의 값과 상관없이 고정된 값을 가져야한다. 그러나 실제 데이터는 독립 변수 값의 크기가 커지면 종속 변수 값의 분산도 커지는 이분산성(heteroskedastic) 문제가 발생한다. 종속변수를 로그 변환한 트랜스로그(translog) 모형을 사용하면 이분산성 문제가 해결되는 경우도 있다.

from sklearn.datasets import load_diabetes

diabetes = load_diabetes()

df = pd.concat([pd.DataFrame(diabetes.data, columns=["x%d" % (i + 1) for i in range(diabetes.data.shape[1])]),

pd.DataFrame(diabetes.target, columns=["target"])],

axis=1)

model = sm.OLS.from_formula("target ~ x9", data=df)

result = model.fit()

plt.scatter(df["x9"], result.resid)

plt.show()

자기 상관 계수#

선형 회귀 모형에서는 오차(disturbance)들이 서로 (모수-조건부) 독립이라고 가정하고 있다. 따라서 잔차(residual)도 서로 독립이어야 한다. 만약 서로 독립이 아니라면 선형회귀 모형이 아닌 ARMA 모형 등의 시계열 모형을 사용해야 한다.

오차가 독립인지 검정하는 방법은 잔차를 시계열로 가정하여 자기상관계수를 구하는 것이다. 만약 독립이라면 시차(lag)가 0인 경우를 제외하고는 자기상관계수 \(\rho_l\) 이 0이어야 한다. 이를 검사하는 검증으로는 다음과 같은 것들이 있다.

Box-Pierce 검정

Ljung-Box 검정

Durbin-Watson 검정

이 검정들은 다음과 같은 귀무 가설을 검증한다.

여기에서는 회귀분석의 성능을 향상시키거나 모형이 가지는 제한조건 등을 충족시키기 위해 모형을 비선형으로 변형(transform)하는 방법에 대해 알아본다.

비선형 변형#

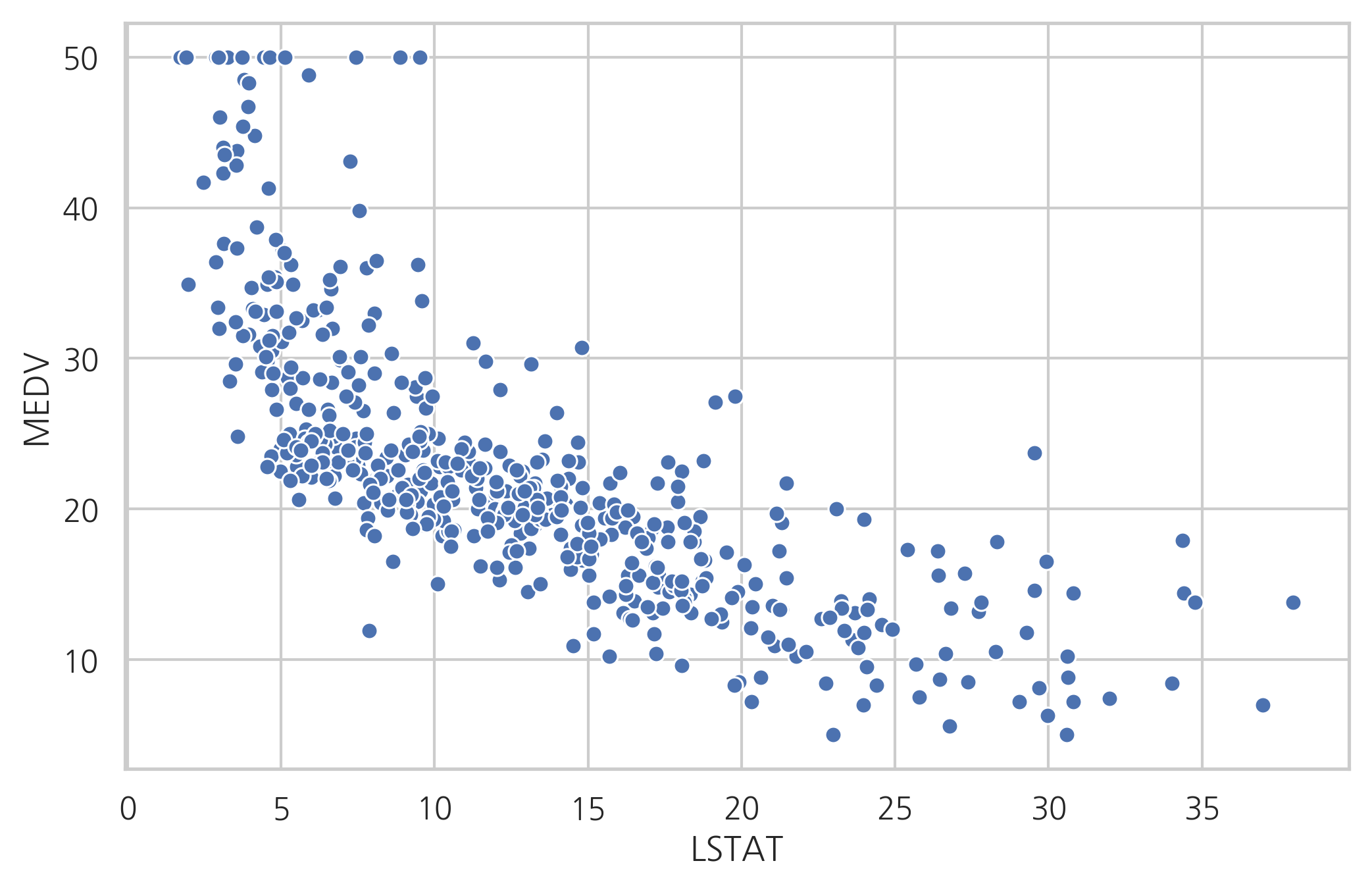

만약 독립변수와 종속변수간의 관계가 비선형이면 이 관계를 선형으로 바꿀 수 있도록 독립변수를 비선형 변환할 수 있다. 예를 들어 보스턴 집값 데이터에서 집값과 LSTAT 데이터는 다음 그림에서 보듯이 비선형 관계를 가진다.

from sklearn.datasets import load_boston

boston = load_boston()

dfX = pd.DataFrame(boston.data, columns=boston.feature_names)

dfy = pd.DataFrame(boston.target, columns=["MEDV"])

df_boston = pd.concat([dfX, dfy], axis=1)

sns.scatterplot(x="LSTAT", y="MEDV", data=df_boston)

plt.show()

이 데이터를 그냥 사용하여 LSTAT과 종속변수간의 선형모형을 구한 결과는 다음과 같다.

model1 = sm.OLS.from_formula("MEDV ~ LSTAT", data=df_boston)

result1 = model1.fit()

print(result1.summary())

OLS Regression Results

==============================================================================

Dep. Variable: MEDV R-squared: 0.544

Model: OLS Adj. R-squared: 0.543

Method: Least Squares F-statistic: 601.6

Date: Mon, 17 Jun 2019 Prob (F-statistic): 5.08e-88

Time: 17:28:28 Log-Likelihood: -1641.5

No. Observations: 506 AIC: 3287.

Df Residuals: 504 BIC: 3295.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 34.5538 0.563 61.415 0.000 33.448 35.659

LSTAT -0.9500 0.039 -24.528 0.000 -1.026 -0.874

==============================================================================

Omnibus: 137.043 Durbin-Watson: 0.892

Prob(Omnibus): 0.000 Jarque-Bera (JB): 291.373

Skew: 1.453 Prob(JB): 5.36e-64

Kurtosis: 5.319 Cond. No. 29.7

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

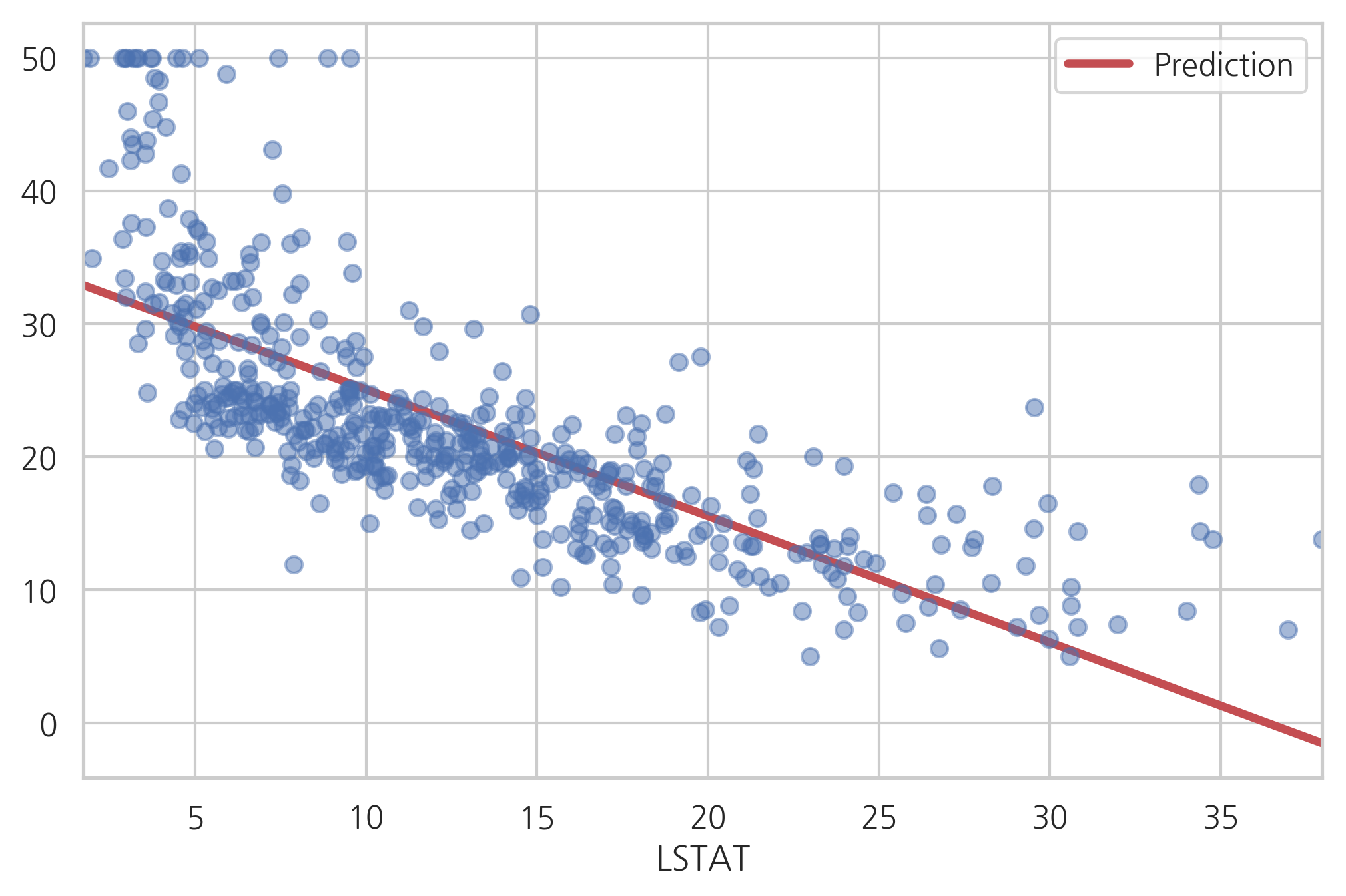

다음 그림은 예측값과 실제 데이터를 비교한 것이다. 선형모형이 적합하지 않음을 알 수 있다.

y_hat1 = result1.predict(df_boston)

df1 = pd.concat([y_hat1, df_boston.LSTAT], axis=1).sort_values("LSTAT")

df1.columns = ["Prediction", "LSTAT"]

df1.plot(x="LSTAT", style="r-", lw=3)

plt.plot(df_boston.LSTAT, df_boston.MEDV, "bo", alpha=0.5)

plt.show()

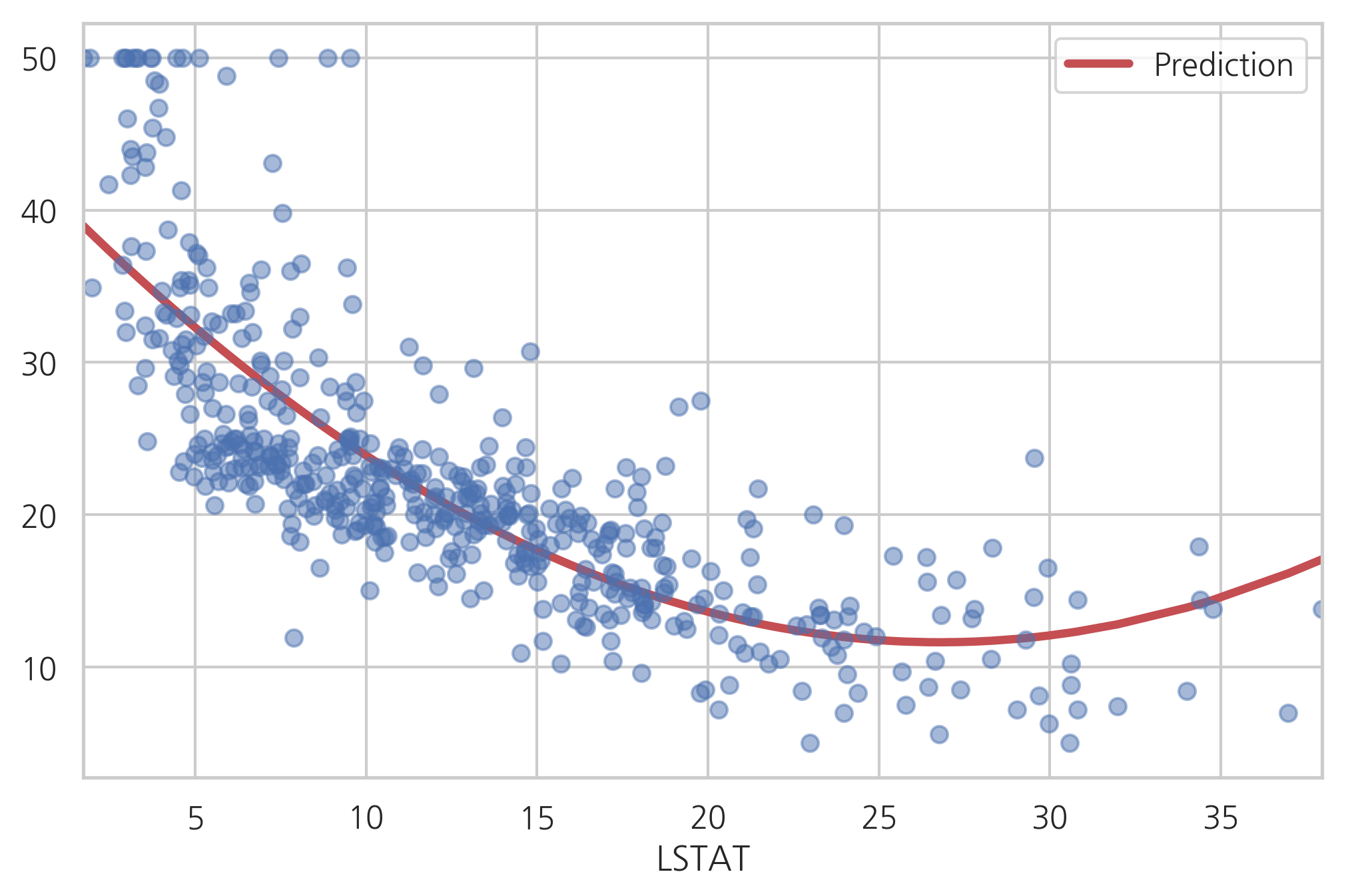

이번에는 LSTAT값을 제곱한 비선형 독립변수를 추가한다. 결과가 향상되었다.

model2 = sm.OLS.from_formula("MEDV ~ LSTAT + I(LSTAT**2)", data=df_boston)

result2 = model2.fit()

print(result2.summary())

OLS Regression Results

==============================================================================

Dep. Variable: MEDV R-squared: 0.641

Model: OLS Adj. R-squared: 0.639

Method: Least Squares F-statistic: 448.5

Date: Mon, 17 Jun 2019 Prob (F-statistic): 1.56e-112

Time: 17:28:28 Log-Likelihood: -1581.3

No. Observations: 506 AIC: 3169.

Df Residuals: 503 BIC: 3181.

Df Model: 2

Covariance Type: nonrobust

=================================================================================

coef std err t P>|t| [0.025 0.975]

---------------------------------------------------------------------------------

Intercept 42.8620 0.872 49.149 0.000 41.149 44.575

LSTAT -2.3328 0.124 -18.843 0.000 -2.576 -2.090

I(LSTAT ** 2) 0.0435 0.004 11.628 0.000 0.036 0.051

==============================================================================

Omnibus: 107.006 Durbin-Watson: 0.921

Prob(Omnibus): 0.000 Jarque-Bera (JB): 228.388

Skew: 1.128 Prob(JB): 2.55e-50

Kurtosis: 5.397 Cond. No. 1.13e+03

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 1.13e+03. This might indicate that there are

strong multicollinearity or other numerical problems.

실제 데이터와 예측값을 비교해보면 선형모형보다 적합한 모형임을 알 수 있다.

y_hat2 = result2.predict(df_boston)

df2 = pd.concat([y_hat2, df_boston.LSTAT], axis=1).sort_values("LSTAT")

df2.columns = ["Prediction", "LSTAT"]

df2.plot(x="LSTAT", style="r-", lw=3)

plt.plot(df_boston.LSTAT, df_boston.MEDV, "bo", alpha=0.5)

plt.show()

범주형을 사용한 비선형성#

독립변수의 비선형성을 포착하는 또 다른 방법 중 하나는 강제로 범주형 값으로 만드는 것이다. 범주형 값이 되면서 독립변수의 오차가 생기지만 이로 인한 오차보다 비선형성으로 얻을 수 있는 이익이 클 수도 있다.

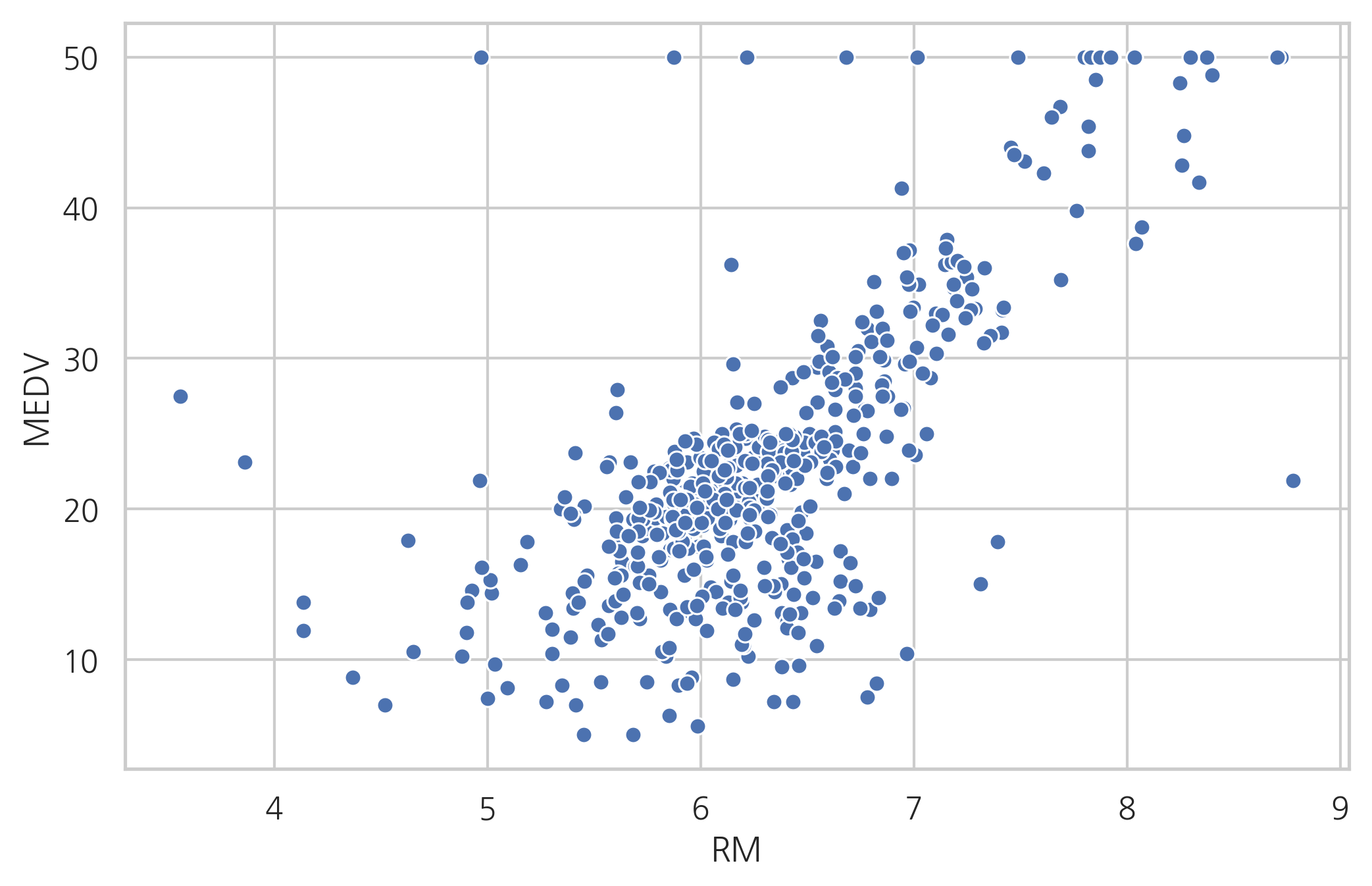

보스턴 집값 데이터에서 종속변수와 RM 변수의 관계는 선형에 가깝지만 방의 갯수가 아주 작아지거나 아주 커지면 선형모형에서 벗어난다.

sns.scatterplot(x="RM", y="MEDV", data=df_boston)

plt.show()

model3 = sm.OLS.from_formula("MEDV ~ RM", data=df_boston)

result3 = model3.fit()

print(result3.summary())

OLS Regression Results

==============================================================================

Dep. Variable: MEDV R-squared: 0.484

Model: OLS Adj. R-squared: 0.483

Method: Least Squares F-statistic: 471.8

Date: Mon, 17 Jun 2019 Prob (F-statistic): 2.49e-74

Time: 17:28:29 Log-Likelihood: -1673.1

No. Observations: 506 AIC: 3350.

Df Residuals: 504 BIC: 3359.

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept -34.6706 2.650 -13.084 0.000 -39.877 -29.465

RM 9.1021 0.419 21.722 0.000 8.279 9.925

==============================================================================

Omnibus: 102.585 Durbin-Watson: 0.684

Prob(Omnibus): 0.000 Jarque-Bera (JB): 612.449

Skew: 0.726 Prob(JB): 1.02e-133

Kurtosis: 8.190 Cond. No. 58.4

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

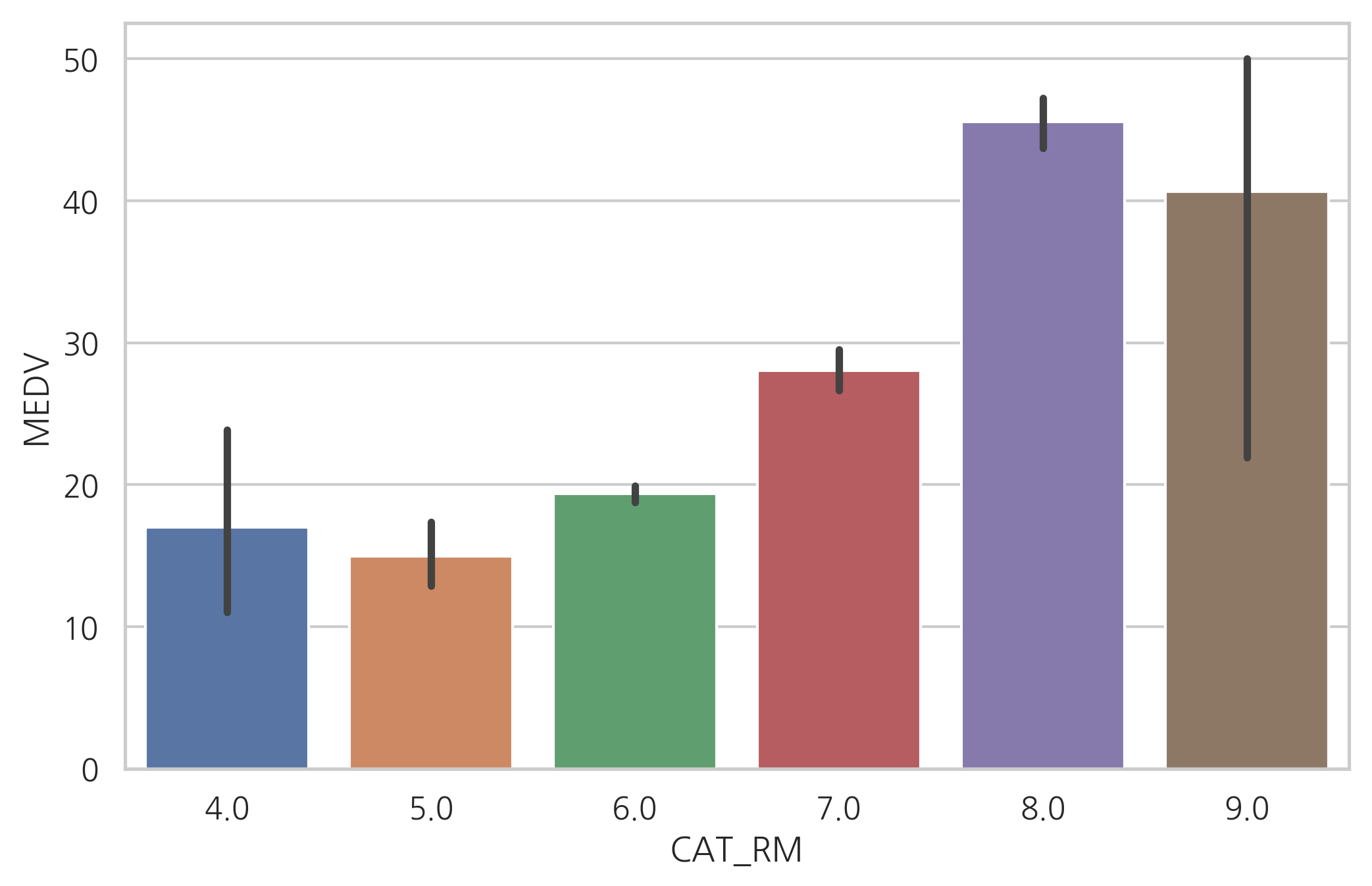

RM 변수값을 강제로 정수로 라운딩(rounding)하면 RM 변수가 가지는 비선형성을 잡을 수 있다. 다음 플롯은 카테고리값으로 변한 RM 변수와 종속변수의 관계를 시각화한 것이다.

rooms = np.arange(3, 10)

labels = [str(r) for r in rooms[:-1]]

df_boston["CAT_RM"] = np.round(df_boston.RM)

sns.barplot(x="CAT_RM", y="MEDV", data=df_boston)

plt.show()

이렇게 하면 RM 변수으로 인한 종속변수의 변화를 비선형 상수항으로 모형화 할 수 있다. 선형모형보다 성능이 향상된 것을 볼 수 있다.

model4 = sm.OLS.from_formula("MEDV ~ C(np.round(RM))", data=df_boston)

result4 = model4.fit()

print(result4.summary())

OLS Regression Results

==============================================================================

Dep. Variable: MEDV R-squared: 0.537

Model: OLS Adj. R-squared: 0.532

Method: Least Squares F-statistic: 115.8

Date: Mon, 17 Jun 2019 Prob (F-statistic): 3.57e-81

Time: 17:28:29 Log-Likelihood: -1645.6

No. Observations: 506 AIC: 3303.

Df Residuals: 500 BIC: 3329.

Df Model: 5

Covariance Type: nonrobust

==========================================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------------------

Intercept 17.0200 2.814 6.049 0.000 11.492 22.548

C(np.round(RM))[T.5.0] -2.0741 2.998 -0.692 0.489 -7.964 3.816

C(np.round(RM))[T.6.0] 2.3460 2.836 0.827 0.409 -3.226 7.918

C(np.round(RM))[T.7.0] 11.0272 2.869 3.843 0.000 5.389 16.665

C(np.round(RM))[T.8.0] 28.5425 3.093 9.228 0.000 22.466 34.619

C(np.round(RM))[T.9.0] 23.6133 4.595 5.139 0.000 14.586 32.641

==============================================================================

Omnibus: 81.744 Durbin-Watson: 0.799

Prob(Omnibus): 0.000 Jarque-Bera (JB): 467.887

Skew: 0.542 Prob(JB): 2.51e-102

Kurtosis: 7.584 Cond. No. 31.1

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

시간 독립변수의 변형#

독립변수가 시간인 경우에는 특정 시점에서 경과된 시간값으로 변형해야 한다. 일간 전기 사용량 데이터를 예로 들어 설명한다.

data = sm.datasets.get_rdataset("elecdaily", package="fpp2")

df_elec = data.data.drop(columns=["WorkDay", "Temperature"])

df_elec["Date"] = pd.date_range("2014-1-1", "2014-12-31")

df_elec.tail()

| Demand | Date | |

|---|---|---|

| 360 | 173.727990 | 2014-12-27 |

| 361 | 188.512817 | 2014-12-28 |

| 362 | 191.273009 | 2014-12-29 |

| 363 | 186.240144 | 2014-12-30 |

| 364 | 186.370181 | 2014-12-31 |

파이썬 datetime 자료형은 toordinal 명령으로 특정 시점으로부터 경과한 시간의 일단위 값을 구하거나 timestamp 메서드로 초단위 값을 구할 수 있다.

import datetime as dt

df_elec["Ordinal"] = df_elec.Date.map(dt.datetime.toordinal)

df_elec["Timestamp"] = df_elec.Date.map(dt.datetime.timestamp)

df_elec.tail()

| Demand | Date | Ordinal | Timestamp | |

|---|---|---|---|---|

| 360 | 173.727990 | 2014-12-27 | 735594 | 1.419606e+09 |

| 361 | 188.512817 | 2014-12-28 | 735595 | 1.419692e+09 |

| 362 | 191.273009 | 2014-12-29 | 735596 | 1.419779e+09 |

| 363 | 186.240144 | 2014-12-30 | 735597 | 1.419865e+09 |

| 364 | 186.370181 | 2014-12-31 | 735598 | 1.419952e+09 |

여기에서는 일단위 시간 값을 사용하여 회귀분석을 한다. 시간 값의 경우 크기가 크므로 반드시 스케일링을 해 주어야 한다.

model5 = sm.OLS.from_formula("Demand ~ scale(Ordinal)", data=df_elec)

result5 = model5.fit()

print(result5.summary())

OLS Regression Results

==============================================================================

Dep. Variable: Demand R-squared: 0.031

Model: OLS Adj. R-squared: 0.028

Method: Least Squares F-statistic: 11.58

Date: Mon, 17 Jun 2019 Prob (F-statistic): 0.000739

Time: 17:28:32 Log-Likelihood: -1709.7

No. Observations: 365 AIC: 3423.

Df Residuals: 363 BIC: 3431.

Df Model: 1

Covariance Type: nonrobust

==================================================================================

coef std err t P>|t| [0.025 0.975]

----------------------------------------------------------------------------------

Intercept 221.2775 1.374 160.997 0.000 218.575 223.980

scale(Ordinal) -4.6779 1.374 -3.404 0.001 -7.381 -1.975

==============================================================================

Omnibus: 43.105 Durbin-Watson: 0.677

Prob(Omnibus): 0.000 Jarque-Bera (JB): 96.485

Skew: 0.614 Prob(JB): 1.12e-21

Kurtosis: 5.199 Cond. No. 1.00

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

하지만 시간 독립변수는 이 외에더 다양한 특징들을 숨기고 있다. 예들 들어 연도, 월, 일, 요일 데이터를 별도의 독립변수로 분리하거나 한 달 내에서 몇번째 날짜인지 월의 시작 또는 끝인지를 나타내는 값은 모두 특징값이 될 수 있다. 판다스에서는 dt 특수 연산자를 사용하여 이러한 값을 구할 수 있다.

df_elec["Year"] = df_elec.Date.dt.year

df_elec["Month"] = df_elec.Date.dt.month

df_elec["DayOfYear"] = df_elec.Date.dt.dayofyear

df_elec["DayOfMonth"] = df_elec.Date.dt.daysinmonth

df_elec["DayOfWeek"] = df_elec.Date.dt.dayofweek

df_elec["WeekOfYear"] = df_elec.Date.dt.weekofyear

df_elec["Weekday"] = df_elec.Date.dt.weekday

df_elec["IsMonthStart"] = df_elec.Date.dt.is_month_start

df_elec["IsMonthEnd"] = df_elec.Date.dt.is_month_end

df_elec.tail()

| Demand | Date | Ordinal | Timestamp | Year | Month | DayOfYear | DayOfMonth | DayOfWeek | WeekOfYear | Weekday | IsMonthStart | IsMonthEnd | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 360 | 173.727990 | 2014-12-27 | 735594 | 1.419606e+09 | 2014 | 12 | 361 | 31 | 5 | 52 | 5 | False | False |

| 361 | 188.512817 | 2014-12-28 | 735595 | 1.419692e+09 | 2014 | 12 | 362 | 31 | 6 | 52 | 6 | False | False |

| 362 | 191.273009 | 2014-12-29 | 735596 | 1.419779e+09 | 2014 | 12 | 363 | 31 | 0 | 1 | 0 | False | False |

| 363 | 186.240144 | 2014-12-30 | 735597 | 1.419865e+09 | 2014 | 12 | 364 | 31 | 1 | 1 | 1 | False | False |

| 364 | 186.370181 | 2014-12-31 | 735598 | 1.419952e+09 | 2014 | 12 | 365 | 31 | 2 | 1 | 2 | False | True |

이렇게 추가적인 특징값을 이용하여 구한 모형은 성능이 향상된다.

feature_names = df_elec.columns.tolist()

feature_names.remove("Demand")

feature_names.remove("Date")

formula = """

Demand ~ scale(Ordinal) + C(Month) + DayOfYear +

C(DayOfMonth) + C(DayOfWeek) + C(Weekday) + C(IsMonthStart) + C(IsMonthEnd)

"""

model6 = sm.OLS.from_formula(formula, data=df_elec)

result6 = model6.fit()

print(result6.summary())

OLS Regression Results

==============================================================================

Dep. Variable: Demand R-squared: 0.537

Model: OLS Adj. R-squared: 0.511

Method: Least Squares F-statistic: 19.98

Date: Mon, 17 Jun 2019 Prob (F-statistic): 4.74e-46

Time: 17:28:32 Log-Likelihood: -1574.8

No. Observations: 365 AIC: 3192.

Df Residuals: 344 BIC: 3273.

Df Model: 20

Covariance Type: nonrobust

===========================================================================================

coef std err t P>|t| [0.025 0.975]

-------------------------------------------------------------------------------------------

Intercept 58.6105 2.423 24.188 0.000 53.844 63.377

C(Month)[T.2] 14.5730 4.587 3.177 0.002 5.551 23.595

C(Month)[T.3] -1.2369 8.663 -0.143 0.887 -18.276 15.802

C(Month)[T.4] -29.1875 10.239 -2.851 0.005 -49.326 -9.049

C(Month)[T.5] 23.4037 15.493 1.511 0.132 -7.069 53.876

C(Month)[T.6] 11.3667 3.758 3.024 0.003 3.974 18.759

C(Month)[T.7] 64.8095 22.750 2.849 0.005 20.063 109.556

C(Month)[T.8] 66.5692 26.490 2.513 0.012 14.467 118.671

C(Month)[T.9] 22.7687 9.491 2.399 0.017 4.100 41.437

C(Month)[T.10] 59.0491 33.895 1.742 0.082 -7.619 125.717

C(Month)[T.11] 33.4276 16.778 1.992 0.047 0.427 66.429

C(Month)[T.12] 72.2523 41.334 1.748 0.081 -9.047 153.552

C(DayOfMonth)[T.30] 38.3755 13.530 2.836 0.005 11.763 64.988

C(DayOfMonth)[T.31] 5.6620 7.806 0.725 0.469 -9.691 21.015

C(DayOfWeek)[T.1] 3.4766 1.829 1.900 0.058 -0.121 7.075

C(DayOfWeek)[T.2] 1.5756 1.821 0.865 0.387 -2.006 5.157

C(DayOfWeek)[T.3] 2.8568 1.831 1.560 0.120 -0.745 6.459

C(DayOfWeek)[T.4] 0.8832 1.831 0.482 0.630 -2.719 4.485

C(DayOfWeek)[T.5] -12.8982 1.831 -7.045 0.000 -16.499 -9.297

C(DayOfWeek)[T.6] -16.4623 1.829 -8.999 0.000 -20.060 -12.864

C(Weekday)[T.1] 3.4766 1.829 1.900 0.058 -0.121 7.075

C(Weekday)[T.2] 1.5756 1.821 0.865 0.387 -2.006 5.157

C(Weekday)[T.3] 2.8568 1.831 1.560 0.120 -0.745 6.459

C(Weekday)[T.4] 0.8832 1.831 0.482 0.630 -2.719 4.485

C(Weekday)[T.5] -12.8982 1.831 -7.045 0.000 -16.499 -9.297

C(Weekday)[T.6] -16.4623 1.829 -8.999 0.000 -20.060 -12.864

C(IsMonthStart)[T.True] 1.2012 5.781 0.208 0.836 -10.169 12.571

C(IsMonthEnd)[T.True] 4.7608 5.781 0.824 0.411 -6.609 16.131

scale(Ordinal) -101.7884 4.209 -24.182 0.000 -110.068 -93.509

DayOfYear 0.6769 0.085 7.926 0.000 0.509 0.845

==============================================================================

Omnibus: 150.460 Durbin-Watson: 0.577

Prob(Omnibus): 0.000 Jarque-Bera (JB): 1586.415

Skew: 1.422 Prob(JB): 0.00

Kurtosis: 12.809 Cond. No. 1.19e+18

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The smallest eigenvalue is 1.14e-29. This might indicate that there are

strong multicollinearity problems or that the design matrix is singular.

주기성을 가지는 독립변수#

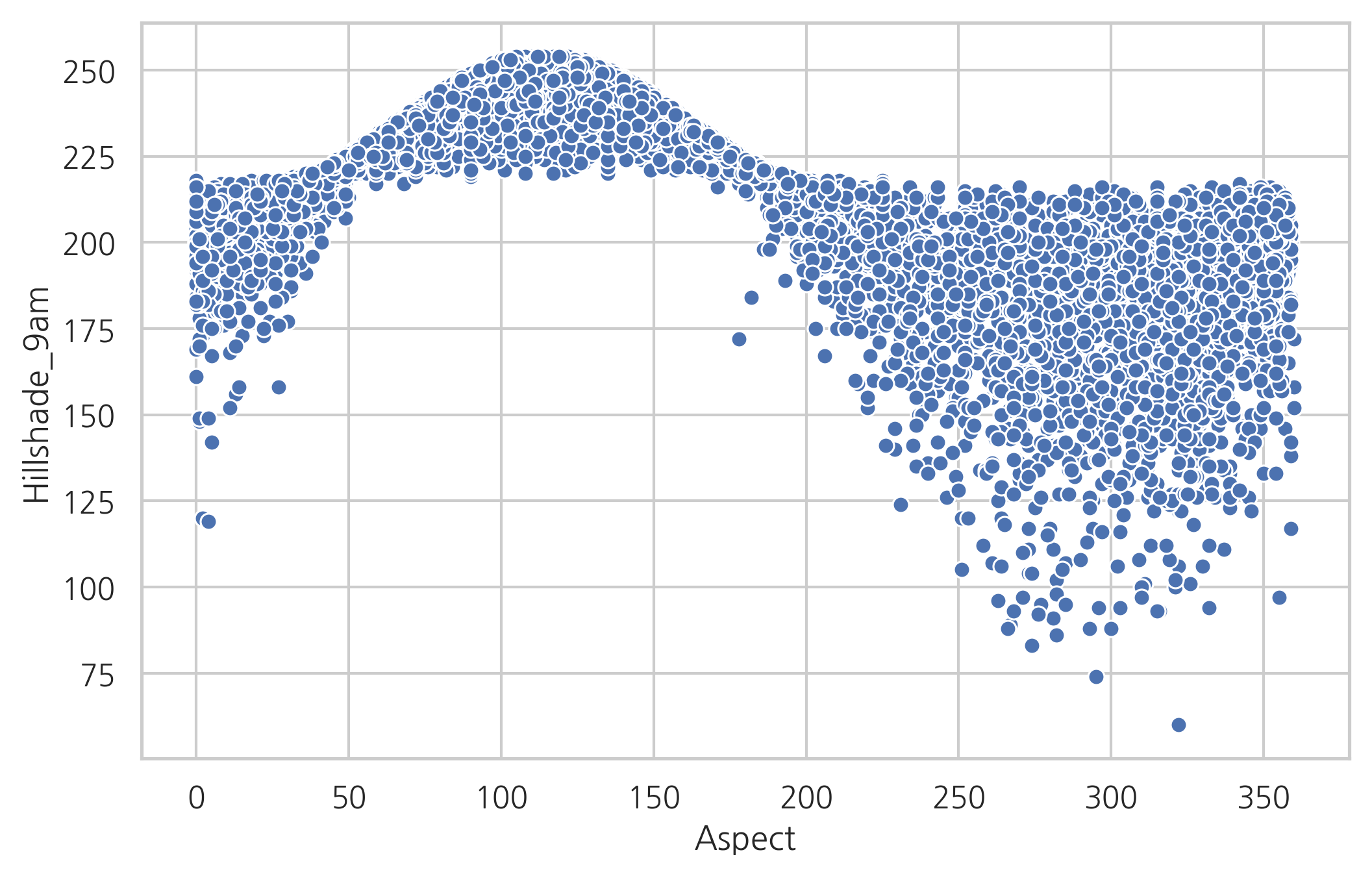

독립변수가 주기성을 가지는 경우에는 그대로 사용하면 모형이 주기성을 가지지 못한다. 예를 들어 scikit-learn의 covtype 데이터를 살펴보자. 이 데이터는 원래 특징값들로부터 특정 범주값을 예측하는 분류 문제용 데이터 집합이지만 Aspect라는 변수를 독립변수로 하고 Hillshade_9am라는 변수를 종속변수로 하는 회귀분석 문제로 가정한다.

from sklearn.datasets import fetch_covtype

covtype = fetch_covtype()

feature_names = ["Aspect", "Hillshade_9am"]

df_covtype = pd.DataFrame(covtype.data[:, [1, 6]], columns=feature_names)

df_covtype = df_covtype.sample(10000, random_state=0) # 편의상 10,000개 표본 추출

df_covtype.tail()

| Aspect | Hillshade_9am | |

|---|---|---|

| 77297 | 90.0 | 235.0 |

| 103214 | 38.0 | 220.0 |

| 459385 | 79.0 | 241.0 |

| 159359 | 58.0 | 225.0 |

| 565783 | 91.0 | 240.0 |

Aspect 변수는 도(degree) 단위의 각도를 나타내는 독립변수이므로 0부터 360까지의 값을 가진다. Aspect가 0인 경우와 360인 경우는 독립변수가 실질적으로 같기 때문에 같은 종속변수값을 예측해야 한다.

sns.scatterplot(x="Aspect", y="Hillshade_9am", data=df_covtype)

plt.show()

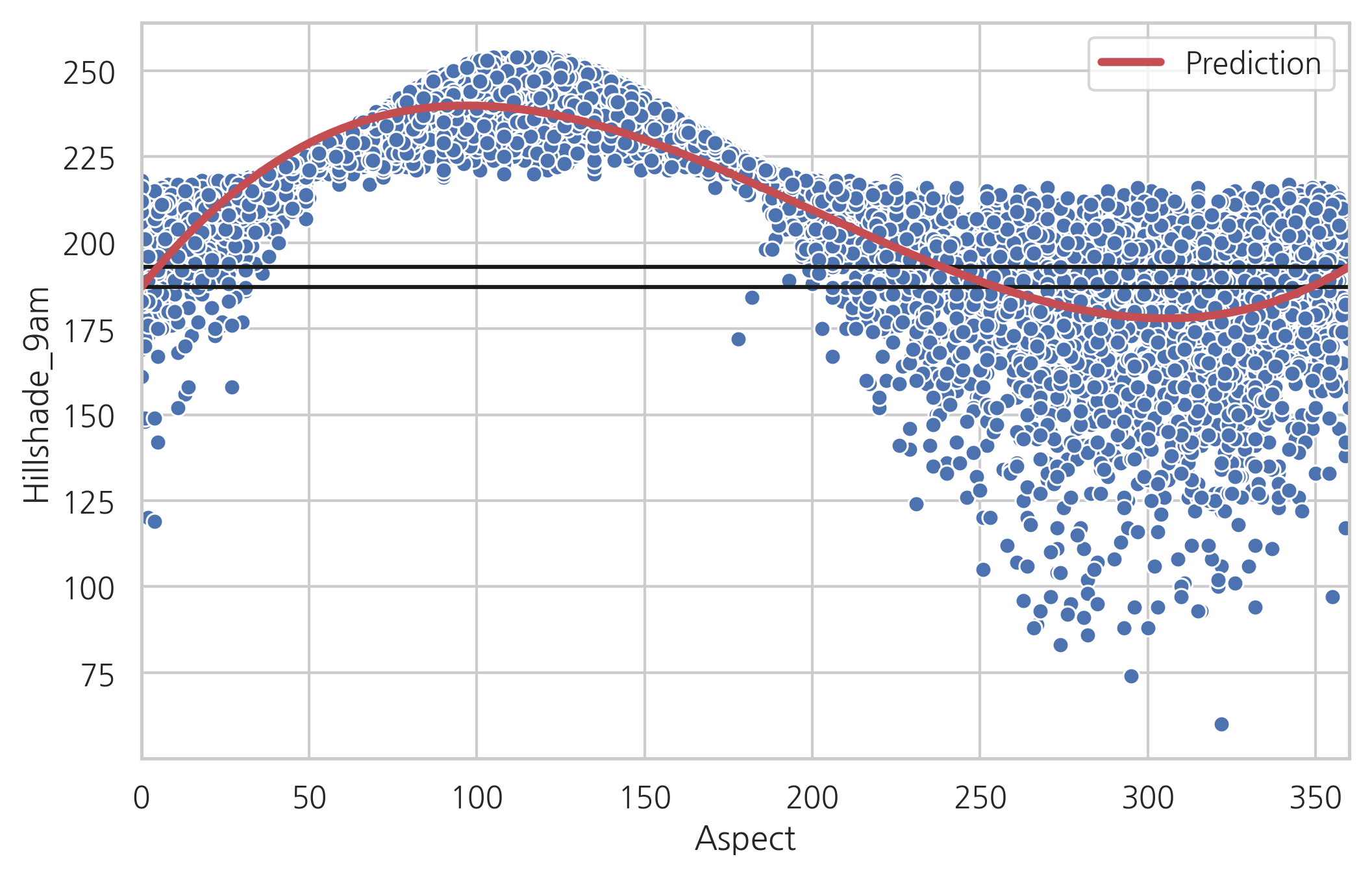

하지만 Aspect를 일반 실수형 독립변수처럼 사용하면 Aspect가 0도일 때와 360도일 때 다른 종속변수값이 예측된다.

model7 = sm.OLS.from_formula(

"Hillshade_9am ~ Aspect + I(Aspect**2) + I(Aspect**3)",

data=df_covtype

)

result7 = model7.fit()

print(result7.summary())

OLS Regression Results

==============================================================================

Dep. Variable: Hillshade_9am R-squared: 0.705

Model: OLS Adj. R-squared: 0.705

Method: Least Squares F-statistic: 7974.

Date: Mon, 17 Jun 2019 Prob (F-statistic): 0.00

Time: 17:28:33 Log-Likelihood: -40905.

No. Observations: 10000 AIC: 8.182e+04

Df Residuals: 9996 BIC: 8.185e+04

Df Model: 3

Covariance Type: nonrobust

==================================================================================

coef std err t P>|t| [0.025 0.975]

----------------------------------------------------------------------------------

Intercept 187.0395 0.485 385.935 0.000 186.089 187.989

Aspect 1.2170 0.013 95.888 0.000 1.192 1.242

I(Aspect ** 2) -0.0083 8.64e-05 -95.669 0.000 -0.008 -0.008

I(Aspect ** 3) 1.369e-05 1.62e-07 84.294 0.000 1.34e-05 1.4e-05

==============================================================================

Omnibus: 3880.162 Durbin-Watson: 1.962

Prob(Omnibus): 0.000 Jarque-Bera (JB): 26433.022

Skew: -1.707 Prob(JB): 0.00

Kurtosis: 10.196 Cond. No. 5.72e+07

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

[2] The condition number is large, 5.72e+07. This might indicate that there are

strong multicollinearity or other numerical problems.

df_test = pd.DataFrame([[0], [360]], columns=["Aspect"])

df_result7 = result7.predict(df_test)

df_result7

0 187.039453

1 193.002560

dtype: float64

y_hat7 = result7.predict(df_covtype)

df7 = pd.concat([y_hat7, df_covtype.Aspect], axis=1).sort_values("Aspect")

df7.columns = ["Prediction", "Aspect"]

df7.plot(x="Aspect", style="r-", lw=3)

sns.scatterplot(x="Aspect", y="Hillshade_9am", data=df_covtype)

plt.hlines(df_result7.values[0], 0, 360)

plt.hlines(df_result7.values[1], 0, 360)

plt.show()

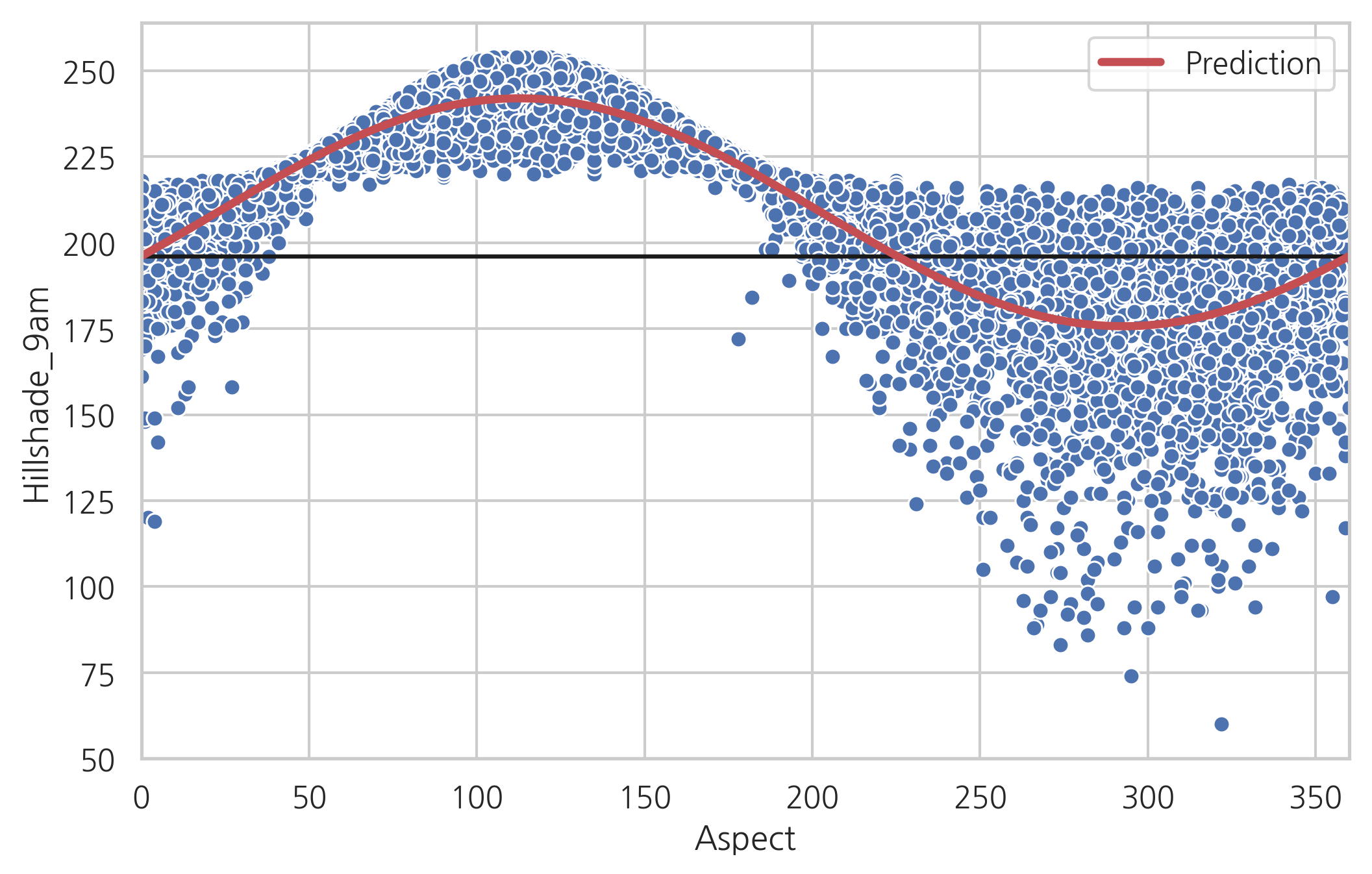

이를 방지하기 위해 일반적으로 주기성을 띄는 독립변수는 다음처럼 두 개의 독립변수로 분리한다.

f = 2.0 * np.pi / 360

model8 = sm.OLS.from_formula("""

Hillshade_9am ~

np.cos(f * Aspect) +

np.sin(f * Aspect)

""", data=df_covtype

)

result8 = model8.fit()

print(result8.summary())

OLS Regression Results

==============================================================================

Dep. Variable: Hillshade_9am R-squared: 0.727

Model: OLS Adj. R-squared: 0.727

Method: Least Squares F-statistic: 1.334e+04

Date: Mon, 17 Jun 2019 Prob (F-statistic): 0.00

Time: 17:28:34 Log-Likelihood: -40515.

No. Observations: 10000 AIC: 8.104e+04

Df Residuals: 9997 BIC: 8.106e+04

Df Model: 2

Covariance Type: nonrobust

======================================================================================

coef std err t P>|t| [0.025 0.975]

--------------------------------------------------------------------------------------

Intercept 208.8444 0.149 1401.376 0.000 208.552 209.137

np.cos(f * Aspect) -12.7745 0.202 -63.281 0.000 -13.170 -12.379

np.sin(f * Aspect) 30.5731 0.206 148.664 0.000 30.170 30.976

==============================================================================

Omnibus: 4129.461 Durbin-Watson: 1.961

Prob(Omnibus): 0.000 Jarque-Bera (JB): 32081.658

Skew: -1.792 Prob(JB): 0.00

Kurtosis: 11.009 Cond. No. 1.66

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

이렇게 하면 독립변수의 특징을 유지하면서 모형이 주기성을 가지게 된다.

df_result8 = result8.predict(df_test)

df_result8

0 196.069868

1 196.069868

dtype: float64

y_hat8 = result8.predict(df_covtype)

df8 = pd.concat([y_hat8, df_covtype.Aspect], axis=1).sort_values("Aspect")

df8.columns = ["Prediction", "Aspect"]

df8.plot(x="Aspect", style="r-", lw=3)

sns.scatterplot(x="Aspect", y="Hillshade_9am", data=df_covtype)

plt.hlines(df_result8.values[0], 0, 360)

plt.hlines(df_result8.values[1], 0, 360)

plt.show()

종속변수 변형#

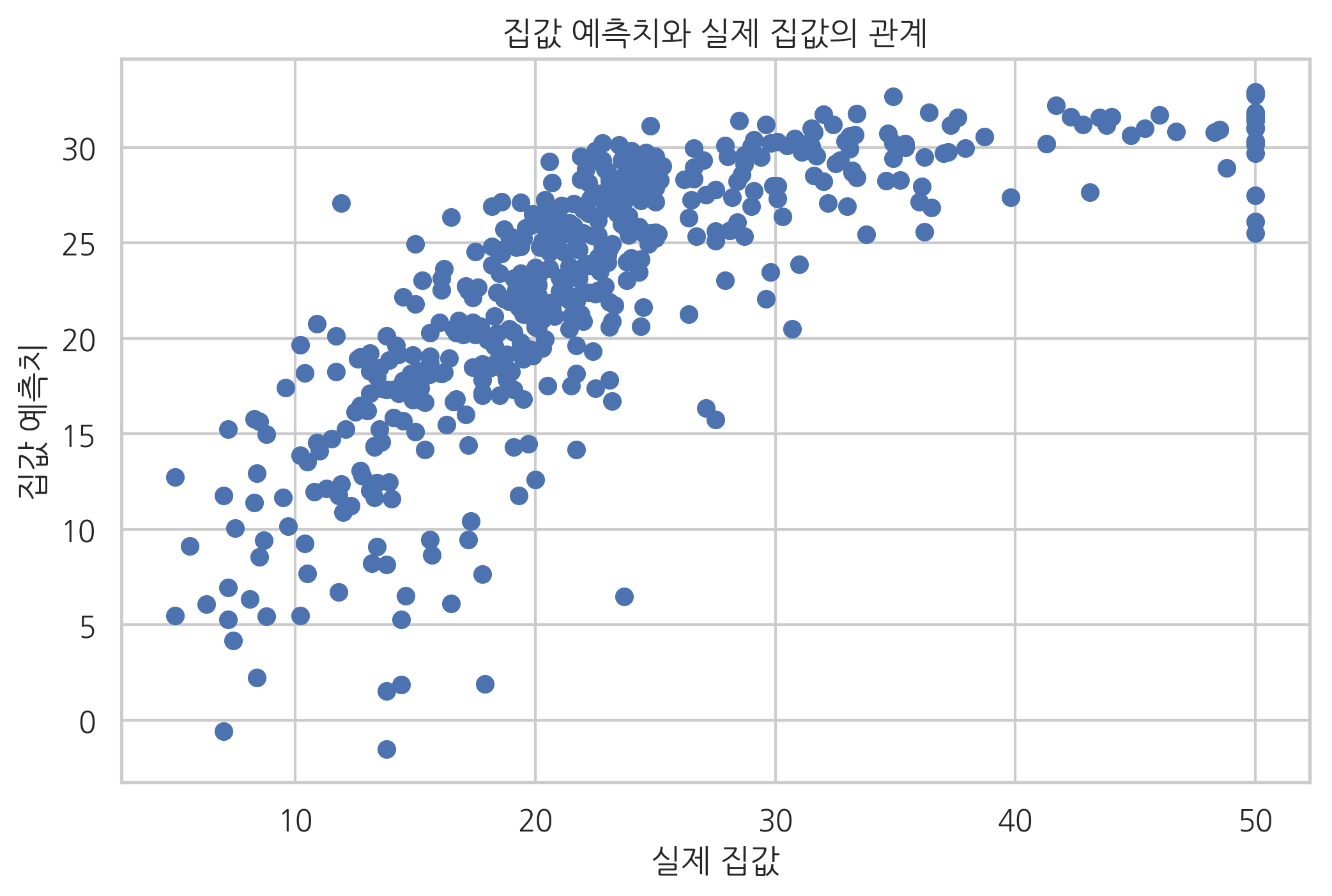

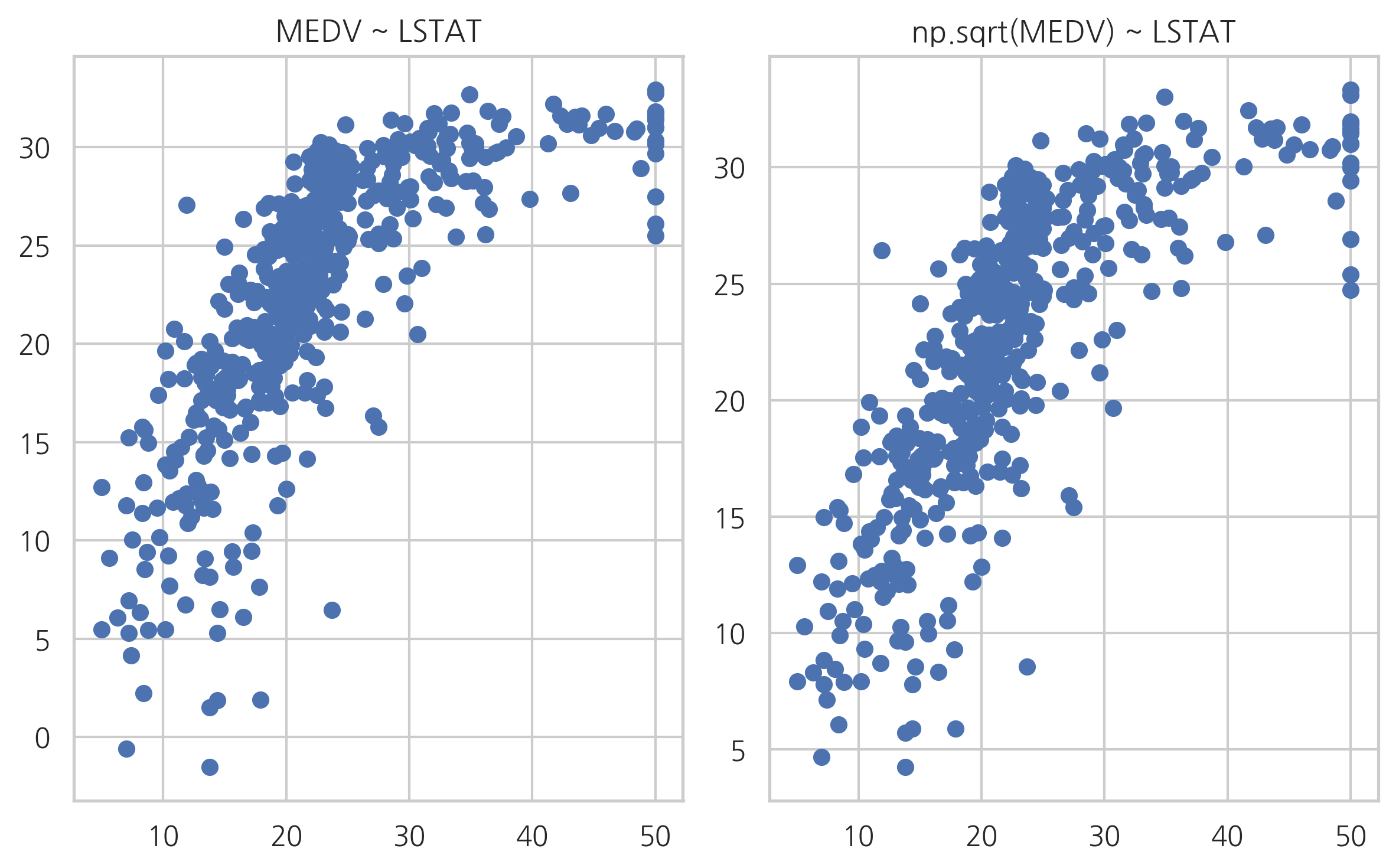

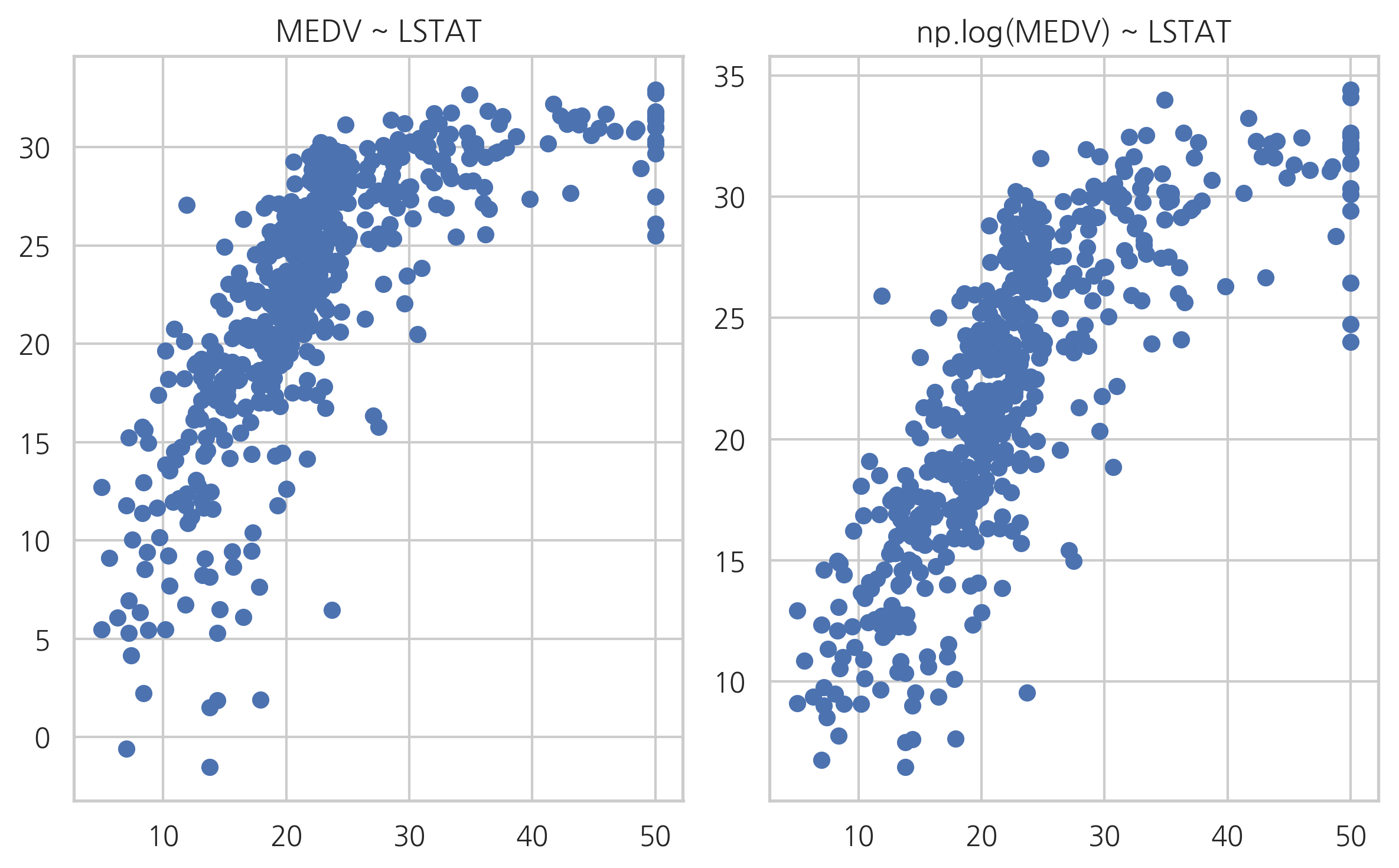

지금까지는 독립변수를 변형하는 방법을 사용했지만 경우에 따라서는 종속변수를 변형할 수도 있다. 예를 들어 LSTAT 독립변수로 보스턴 집값을 예측하는 선형회귀모형의 예측값과 실제값을 그리면 다음과 같다.

plt.scatter(boston.target, y_hat1)

plt.xlabel(u"실제 집값")

plt.ylabel(u"집값 예측치")

plt.title("집값 예측치와 실제 집값의 관계")

plt.show()

모형이 올바르다면 예측치와 실제 종속변수값을 그린 스캐터 플롯은 선형적인 모습이 나와야 한다. 하지만 실제로는 제곱근이나 로그 그래프와 더 유사하다. 이러한 경우에는 이 스캐터 플롯을 선형적으로 만들어 주도록 예측치를 비선형 변환한다. 여러가지 모형을 비교해보면 독립변수와 종속변수를 모두 로그 변환한 모형이 가장 좋다는 것을 알 수 있다.

model11 = sm.OLS.from_formula("np.sqrt(MEDV) ~ LSTAT", data=df_boston)

result11 = model11.fit()

print(result11.summary())

OLS Regression Results

==============================================================================

Dep. Variable: np.sqrt(MEDV) R-squared: 0.610

Model: OLS Adj. R-squared: 0.610

Method: Least Squares F-statistic: 789.7

Date: Mon, 17 Jun 2019 Prob (F-statistic): 3.09e-105

Time: 17:28:35 Log-Likelihood: -445.65

No. Observations: 506 AIC: 895.3

Df Residuals: 504 BIC: 903.7

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 5.9499 0.053 112.374 0.000 5.846 6.054

LSTAT -0.1024 0.004 -28.101 0.000 -0.110 -0.095

==============================================================================

Omnibus: 74.833 Durbin-Watson: 0.900

Prob(Omnibus): 0.000 Jarque-Bera (JB): 111.528

Skew: 0.976 Prob(JB): 6.05e-25

Kurtosis: 4.216 Cond. No. 29.7

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

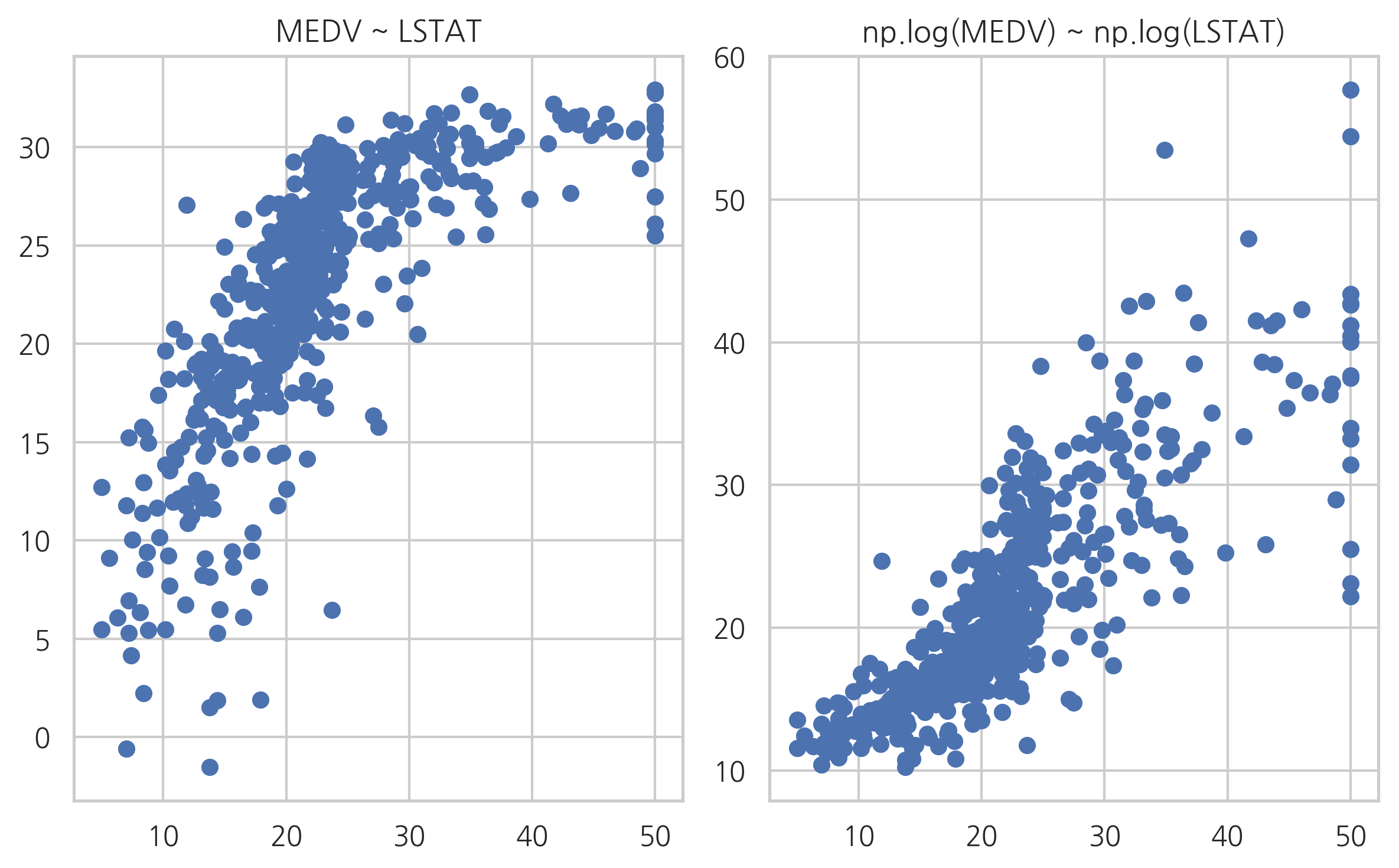

plt.subplot(121)

plt.scatter(boston.target, y_hat1)

plt.title("MEDV ~ LSTAT")

plt.subplot(122)

plt.scatter(boston.target, (result11.predict(df_boston))**2)

plt.title("np.sqrt(MEDV) ~ LSTAT")

plt.tight_layout()

plt.show()

model12 = sm.OLS.from_formula("np.log(MEDV) ~ LSTAT", data=df_boston)

result12 = model12.fit()

print(result12.summary())

OLS Regression Results

==============================================================================

Dep. Variable: np.log(MEDV) R-squared: 0.648

Model: OLS Adj. R-squared: 0.647

Method: Least Squares F-statistic: 928.1

Date: Mon, 17 Jun 2019 Prob (F-statistic): 2.23e-116

Time: 17:28:35 Log-Likelihood: -0.57634

No. Observations: 506 AIC: 5.153

Df Residuals: 504 BIC: 13.61

Df Model: 1

Covariance Type: nonrobust

==============================================================================

coef std err t P>|t| [0.025 0.975]

------------------------------------------------------------------------------

Intercept 3.6176 0.022 164.654 0.000 3.574 3.661

LSTAT -0.0461 0.002 -30.465 0.000 -0.049 -0.043

==============================================================================

Omnibus: 27.562 Durbin-Watson: 0.909

Prob(Omnibus): 0.000 Jarque-Bera (JB): 50.719

Skew: 0.351 Prob(JB): 9.69e-12

Kurtosis: 4.383 Cond. No. 29.7

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

plt.subplot(121)

plt.scatter(boston.target, y_hat1)

plt.title("MEDV ~ LSTAT")

plt.subplot(122)

plt.scatter(boston.target, np.exp(result12.predict(df_boston)))

plt.title("np.log(MEDV) ~ LSTAT")

plt.tight_layout()

plt.show()

model13 = sm.OLS.from_formula("np.log(MEDV) ~ np.log(LSTAT)", data=df_boston)

result13 = model13.fit()

print(result13.summary())

OLS Regression Results

==============================================================================

Dep. Variable: np.log(MEDV) R-squared: 0.677

Model: OLS Adj. R-squared: 0.677

Method: Least Squares F-statistic: 1058.

Date: Mon, 17 Jun 2019 Prob (F-statistic): 7.32e-126

Time: 17:28:36 Log-Likelihood: 21.325

No. Observations: 506 AIC: -38.65

Df Residuals: 504 BIC: -30.20

Df Model: 1

Covariance Type: nonrobust

=================================================================================

coef std err t P>|t| [0.025 0.975]

---------------------------------------------------------------------------------

Intercept 4.3618 0.042 103.603 0.000 4.279 4.445

np.log(LSTAT) -0.5598 0.017 -32.521 0.000 -0.594 -0.526

==============================================================================

Omnibus: 24.565 Durbin-Watson: 0.855

Prob(Omnibus): 0.000 Jarque-Bera (JB): 58.236

Skew: -0.205 Prob(JB): 2.26e-13

Kurtosis: 4.611 Cond. No. 11.5

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

plt.subplot(121)

plt.scatter(boston.target, y_hat1)

plt.title("MEDV ~ LSTAT")

plt.subplot(122)

plt.scatter(boston.target, np.exp(result13.predict(df_boston)))

plt.title("np.log(MEDV) ~ np.log(LSTAT)")

plt.tight_layout()

plt.show()